LOCAL: +61 (0) 412 366 570

Stewards FMG Pty Ltd © 2014 | Privacy policy

Helping families and trustees build and protect wealth for beneficiaries

Advice and Guidance for your Family and your Family Office

Happiest Clients

The happiest clients I ever met was a retired couple in their late 80’s living on a tiny pension and $30,000 in the bank.

They had sold their home, bought a caravan and had no fixed address…and I still blush when I think about how affectionate they were with each other during the meeting.

I wanted to start with this eye witness account as a testament to the fact that you don’t need wealth to be happy.

Most people know that money…and its accumulation is simply a means to an end; not an end in itself.

In other words for many of my clients the enjoyment derived from their wealth doesn’t come from the accumulation of money but the spending of it.

What’s on your “bucket list”?

After 25 years as an adviser I have witnessed a vast array of “bucket list” items some of the more notable of which have included:

• buying an oyster farm;

• creating a charitable trust;

• becoming an eBay trader and

• collecting and trading vintage fountain pens.

As an aside, my oyster farmer ended up making more money in retirement than he did when he worked and he was by far and away the most enjoyable client when it came to our bi-annual reviews.

After sitting down in my office he would start with “what would you like today…red or white”. After making my selection he would reach into his bag and bring out the appropriate bottle of wine, two glasses and a couple of dozen unchucked oysters.

I distinctly remember another couple who used to agonise over their wealth…he wanted to spend it but she couldn’t bring herself to buy a new dress despite the fact that they had plenty.

For these clients part of my job was convincing her that they had enough money for at least 2 or 3 rainy days and they would be hard pressed to put a dent in their wealth no matter how many trips or dresses they had.

Champagne lifestyle planned for a beer budget?

In many instances my job at some point is to convince the client that the champagne lifestyle they had planned for themselves can’t be funded with their “beer” resources.

Let me recount a recent client meeting with some of the details changed of course to keep things private.

For example …

I met with Mal and Lyn a few months ago. A couple in their early 60’s, Lyn had retired a year earlier but Mal still worked part time 3 days a week and intended to do so for another couple of years. Their after tax, annual living costs was about $1,000 a week.

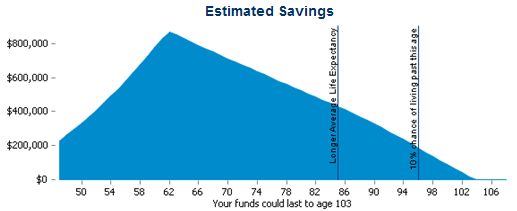

In retirement they clearly stated that they wanted to keep funding their lifestyle at this level and after we added into the mix their savings of $980,000 it looked as though this was very achievable. In fact it looked as though the money would never run out.

Clearly they were very happy with this projection particularly in view of the fact that it could be achieved with relatively low levels of investment risk.

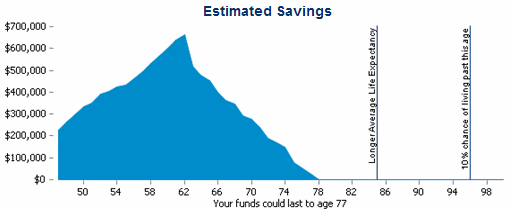

Our conversation soon shifted toward all the pent up plans and goals they had for themselves. Without going through an exhaustive list, their headline items included:

• Taking an overseas holiday for 3 months at a time every 2 years at an estimated cost of $35,000 per trip.

• Paying their grandchild’s university fees for 5 years at a cost of $25,000 a year; and

• Replacing their family car every 3 years at a cost of approximately $20,000 every time they did a change over.

With the addition of just these three items, their expectations came crashing back to earth.

To get them back on track it took a few small adjustments to get them back on track namely:

• reducing their living cost by just $100 per week,

• increasing their annual investment return target from 1% to 2% above inflation; and

• the cost and frequency of some of the big ticket items,

What this process did?

Firstly Mal and Lyn now knew how much lifestyle their wealth could deliver to them.

Secondly and most importantly, they now understood that a key part of enjoying their wealth was in the knowing.